Planning is a most critical element in any Section 1031 exchange.

It is extremely important for taxpayers to contact IPE 1031 prior to undertaking a Section 1031 tax-deferred exchange. Taxpayers must structure Section 1031 transactions so they meet the requirements of the Internal Revenue Code. At a minimum, taxpayers should contact IPE 1031 as soon as possible, and prior to closing on the sale of their relinquished property(ies).

Taxpayers desiring to execute an I.R.C. Section 1031 exchange should include cooperation and assignability language in the relinquished and replacement property purchase and sale agreements. IPE 1031 will provide exchanging taxpayers and/or their tax/legal advisors with suggested language for the Purchase and Sale Agreement detailing the taxpayer’s intent to execute a Section 1031 exchange.

IPE 1031 will consult with the taxpayer and/or the taxpayer’s team of tax/legal advisors to aid in the successful implementation of the exchange. Step-by-step, detailed instructions are provided to each client and to the client’s advisors.

PLEASE NOTE: Careful attention must be paid by the exchanging taxpayer to ensure that a qualified intermediary has been retained prior to the sale of the relinquished property. Closing on the relinquished property cannot occur without the prior execution of appropriate exchange documents. The taxpayer, nor the taxpayer’s agents, can receive any of the proceeds from the sale. Further, absent additional planning and documentation, it is not possible to close on the purchase of replacement property prior to closing the sale of the relinquished property. In this case, a reverse exchange must be implemented. Please contact IPE 1031 for more information if you are considering a reverse exchange transaction.

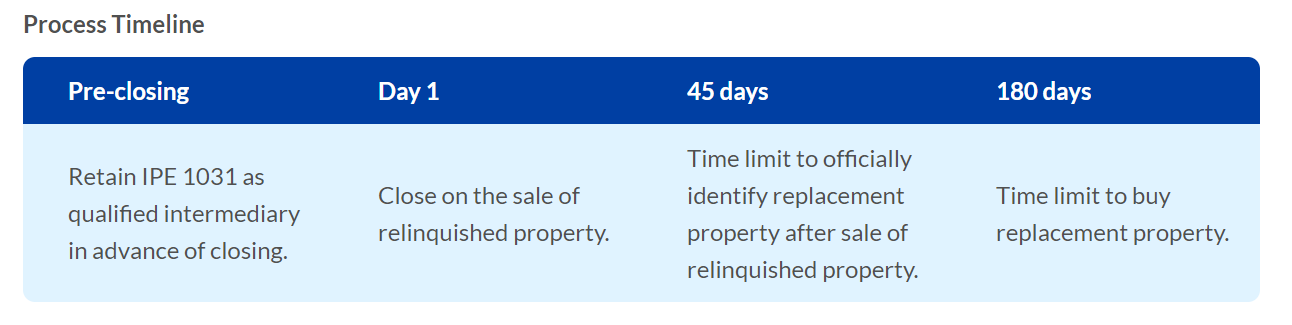

Process Timeline

Pre-closing

- Retain IPE 1031 as qualified intermediary in advance of closing.

Day 1

- Close on the sale of relinquished property.

45 days

- Time limit to officially identify replacement property after sale of relinquished property

180 days

- Time limit to buy replacement property.

Download the timeline table as an image to print.

{kind=link}

WASHINGTON STATE REQUIRED NOTICE: WASHINGTON STATE LAW, RCW 19.310.040, REQUIRES AN EXCHANGE FACILITATOR TO EITHER MAINTAIN A FIDELITY BOND IN AN AMOUNT OF NOT LESS THAN ONE MILLION DOLLARS THAT PROTECTS CLIENTS AGAINST LOSSES CAUSED BY CRIMINAL ACTS OF THE EXCHANGE FACILITATOR, OR TO HOLD ALL CLIENT FUNDS IN A QUALIFIED ESCROW ACCOUNT OR QUALIFIED TRUST THAT REQUIRES YOUR CONSENT FOR WITHDRAWALS. ALL EXCHANGE FUNDS MUST BE DEPOSITED IN A SEPARATELY IDENTIFIED ACCOUNT USING YOUR TAXPAYER IDENTIFICATION NUMBER. YOU MUST RECEIVE WRITTEN NOTIFICATION OF HOW YOUR EXCHANGE FUNDS HAVE BEEN DEPOSITED. YOUR EXCHANGE FACILITATOR IS REQUIRED TO PROVIDE YOU WITH WRITTEN DIRECTIONS OF HOW TO INDEPENDENTLY VERIFY THE DEPOSIT OF THE EXCHANGE FUNDS. EXCHANGE FACILITATION SERVICES ARE NOT REGULATED BY ANY AGENCY OF THE STATE OF WASHINGTON OR OF THE UNITED STATES GOVERNMENT. IT IS YOUR RESPONSIBILITY TO DETERMINE THAT YOUR EXCHANGE FUNDS WILL BE HELD IN A SAFE MANNER.